When Private-Equity Firms Bankrupt Their Own Companies

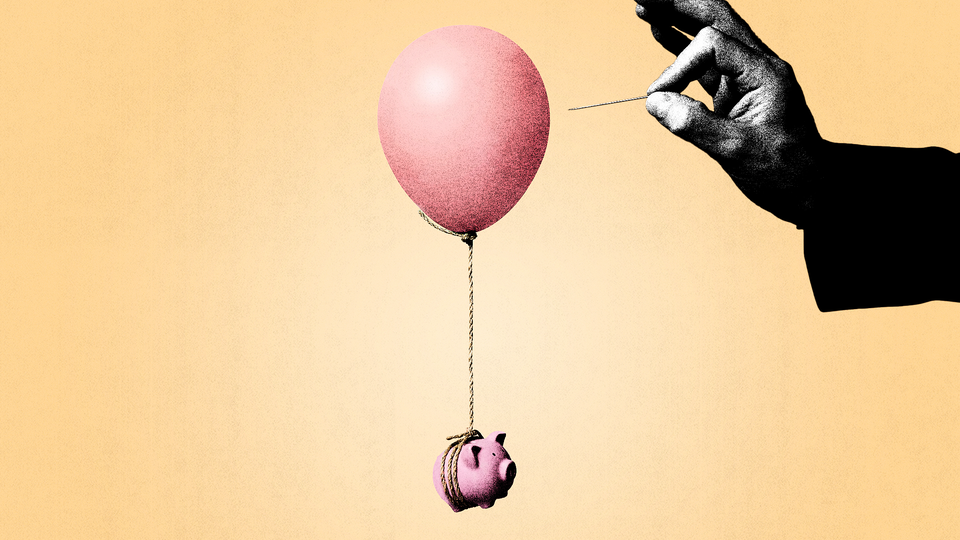

Private-equity firms can succeed when their companies, customers, and employees fail. It’s a broken system.

Private-equity firms buy businesses in the hopes of flipping them for a profit a few years later. The idea is simple enough. But companies bought by private-equity firms are 10 times as likely to go bankrupt as those that aren’t. The industry’s defenders claim that this is simply because private-equity firms often buy teetering companies; no wonder, then, that a disproportionate number fail. Besides, they say, no firm wants its business to go bankrupt.

But what if that weren’t true? What if private-equity firms not only tolerated but profited from the bankruptcy of their companies? (Here, I write in my personal capacity, and my views do not necessarily reflect those of the Department of Justice.)

Consider the case of Friendly’s. The ice-cream-and-diner chain was started by two brothers, Curtis and S. Prestley Blake, in the depths of the Great Depression. The Blake brothers ran the business as a family affair: Their mother made their coffee-flavored syrup, and each night, one brother would stay up making ice cream for the next day while the other slept. Through hard work, the Blakes succeeded, and from their first store they expanded to a second, and then to a third. When the United States entered World War II, the brothers closed their shop, saying that they would reopen “when we win the war”; when they did, they turned their business into a regional dining institution with dozens of locations across the Northeast.

When the Blake brothers finally retired, Friendly’s cycled through a series of owners until 2007, when it was acquired by the private-equity firm Sun Capital. Under Capital’s ownership, Friendly’s struggled. Among other things, the private-equity firm piled debt onto the business, and required it to sell and lease back the property for some 160 restaurants, a move that made a quick profit but saddled Friendly’s with a new, unending obligation. Ultimately, Sun Capital pushed the chain into bankruptcy.

If Sun Capital showed no great aptitude for running Friendly’s, it demonstrated enormous skill in directing its bankruptcy. Under Sun Capital’s ownership, Friendly’s steered the case to Delaware—generally a favorable district for corporations—by chartering several subsidiaries there. Then Friendly’s lawyers successfully petitioned to expedite the bankruptcy process through a “363 sale,” in which the company’s assets—or the company itself—are auctioned off free of its prior debts. The process largely removes the discretion of the court and, in Friendly’s case, gave the chain greater leeway to choose who would buy it. (One judge complained that, in such auctions, the judge “might as well leave his or her signature stamp with the debtor’s counsel and go on vacation.”)

And here’s where private equity showed its genius. Sun Capital, through Friendly’s, proposed to sell the business to … itself. It was able to do this by becoming not just the chain’s largest owner, but also its largest lender, with hundreds of millions of dollars in unpaid debts. Sun Capital proposed to reacquire Friendly’s by forgiving these debts, a tactic known as “credit bidding.” Other potential acquirers were at a huge disadvantage, as they’d have to bid real money against the debts to Sun Capital, which were worth a fraction of their stated value. Nobody else could hope to pay so little for so much. And nobody did. An auction for the company was canceled for lack of interest. Sun Capital’s subsidiary was able to acquire Friendly’s without a fight.

But why go through this complicated process? Why would Friendly’s declare bankruptcy just to be sold from one Sun Capital fund to another? The answer was simple: pensions. At the time of bankruptcy, Friendly’s had $115 million in pension liabilities. By selling Friendly’s to one of its affiliates, Sun Capital reacquired its own company free and clear of those liabilities. These debts were pushed onto the Pension Benefit Guaranty Corporation (PBGC), a government-chartered insurer that rescues underfunded pensions, and whose work was paid for by other, more responsible, pension funds.

Sun Capital was able to reacquire Friendly’s free of its pension obligations, without spending anything more than the money it had already lent out. Pensioners lost in this process because their payments were at risk of being cut. Many of the chain’s existing employees lost as well: 63 restaurants closed as part of the bankruptcy process. The Blake brothers lost too. Both men—who’d closed their business during World War II until “we win the war”—lived long enough to see their creation collapse at the hands of Sun Capital. But Sun Capital’s co-founder demonstrated no comparable patriotism or seriousness of purpose. When asked by The New York Times in 2012 about the failure of Friendly’s and his arguable manipulation of the bankruptcy law, he said, “We don’t make the rules.”

Friendly’s wasn’t Sun Capital’s only victim. The firm similarly pushed the Midwest grocer Marsh Supermarket into bankruptcy. At the time, Marsh owed $62 million in pension obligations to its warehouse workers, plus millions more to its store employees. (A separate fund for the company’s executives remained fully funded.) Through bankruptcy, Sun Capital was able to offload Marsh’s unfunded pension obligations onto the PBGC, which ultimately had to cut benefits for warehouse workers by a quarter. Sun Capital engaged in similar “pension laundering,” in the words of a former PBGC director, with the aluminum-parts maker Indalex and the generator manufacturer Powermate. For its part, Sun Capital told The Washington Post in 2018 that its investment in Marsh “kept the company alive,” and that Indalex’s and Powermate’s “significant” pension debts predated its purchase of either. Yet even if that’s true, Sun Capital showed a recurring enthusiasm for abandoning the pensions of the companies it bought.

Other private-equity firms play this game too. When Wasserstein & Co. and Highfields Capital Management LP bought the specialty-food retailer Harry & David, they also forced the company into bankruptcy and pushed pension obligations onto the PBGC, but not before giving themselves $80 million in dividends. (After Harry & David went bankrupt, the CEO of Wasserstein defended its acquisition to Bloomberg in 2011, saying that the debt it put on the company was comparatively small.) Similarly, the private-equity firm Yucaipa and its partners bought the grocer A&P out of bankruptcy, and sent it back just a few years later, pushing the company’s pension obligations onto the PBGC in the process. (When it declared bankruptcy a second time, A&P said that it “did not achieve nearly as much as was needed to turn around its business.”) In all, according to a 2015 Harvard study, private-equity firms had pushed more than 50 companies into bankruptcy and sloughed off to the PBGC more than $1.5 billion in obligations since 2001. In the process, pensioners lost $128 million in benefits.

This system, which allows private-equity firms to succeed when their companies, customers, and employees fail, is broken. It also can be fixed. Congress can revise the bankruptcy code to limit the use of firms’ preferred tactics, such as forum shopping, credit bidding, and 363 sales. Activists and bankruptcy lawyers can also help make the case—both to the public and to courts—that these tactics can hurt ordinary people, a truth often obscured by the arcana of the bankruptcy process. Such activism, education, and outreach can have a real effect on these courts and even Congress. It’s crucial work, for without it, the tactics that private-equity firms used on companies such as Friendly’s may someday be used on yours.

This article was adapted from Ballou’s forthcoming book, Plunder: Private Equity’s Plan to Pillage America.