Health Insurance and the American Public

The great expansion of voluntary health insurance in recent years is part of a significant but little not iced social and economic transformation in the United States. The president of the Health Insurance Association of America tells how the insurance companies have pioneered in the development of sound principles and techniques of protecting millions of families and individuals against the high cost of ill health and loss of income.

By E. J. FAULKNER

President, Health Insurance Association of America

Since 1941—in a short span of sixteen years— the American people have witnessed some of the most phenomenal social and economic changes in the entire history of our country. In keeping with our democratic way of life these developments have found public favor only when they provided a service or product that was desired by most of us.

The financing of health care is an outstanding example of a social need which American business has been striving to meet through the development of voluntary health insurance. In 1941, voluntary health insurance was comparatively unknown to the majority of American people.

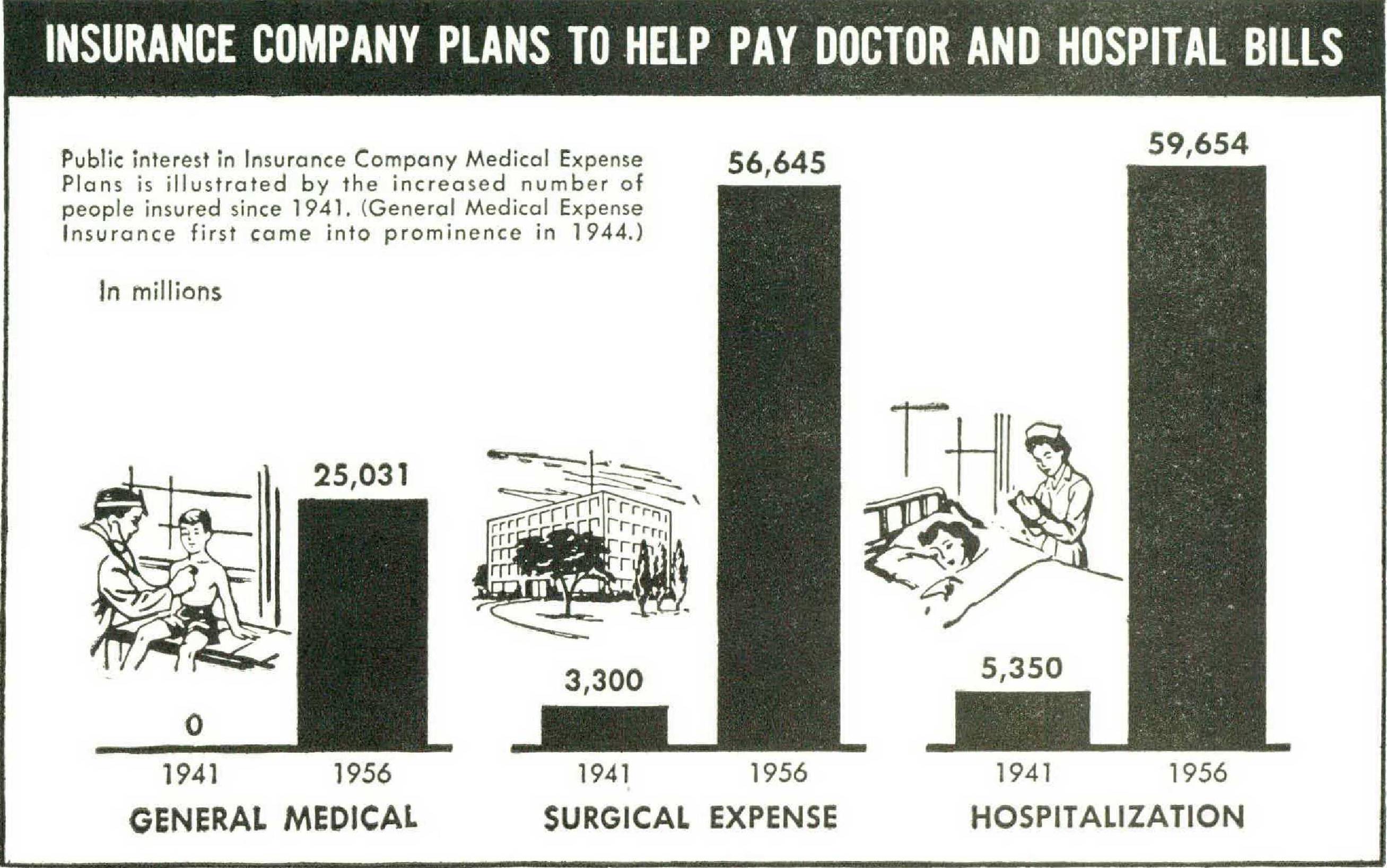

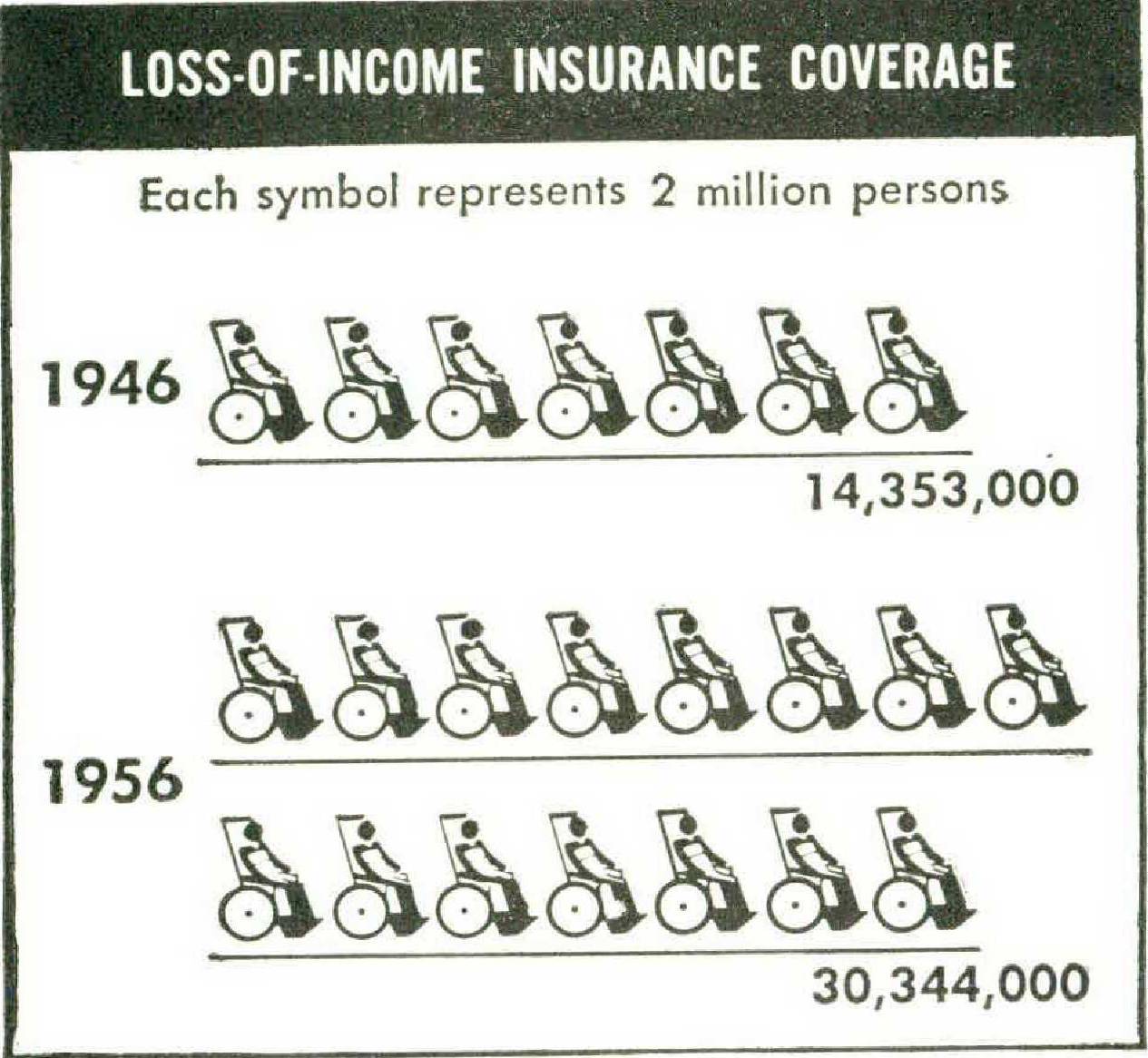

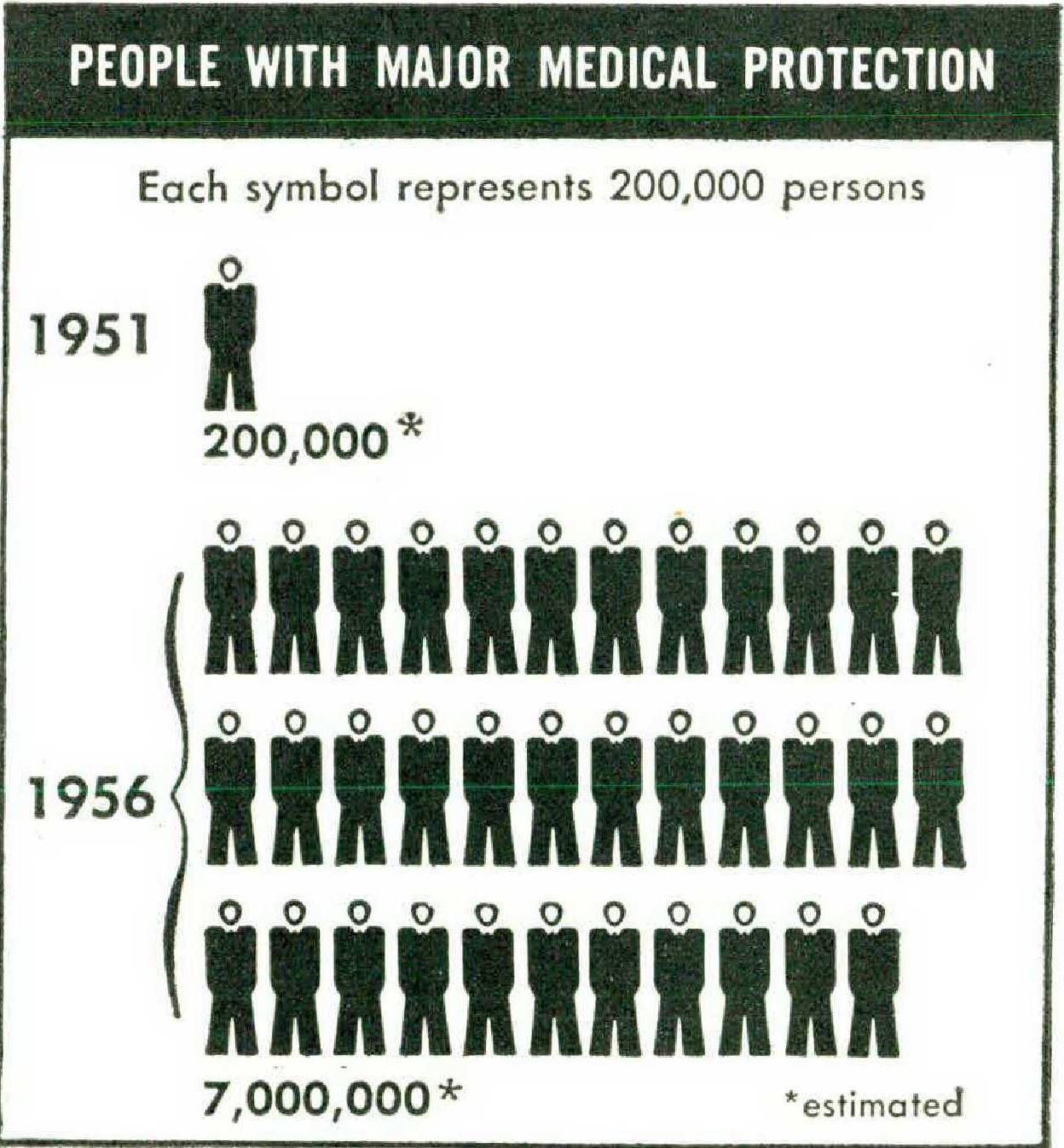

Today, voluntary hospital insurance alone protects 110 million Americans; 94 million have insurance against surgical expense; 58 million against general medical expense; and seven million are insured by the newest and broadest health protection available—major medical expense insurance introduced just six years ago. In addition, close to two-thirds of all gainfully employed civilians in this country participate in some plan enabling them to continue their income during a period of disability.

Considered in another light, the extraordinarily rapid growth of voluntary health insurance since 1941 shows that the number of people protected by hospital insurance has increased 600 per cent; surgical insurance 1,300 per cent; and general medical insurance 1,700 per cent. Since 1951, when major medical expense insurance was introduced, its volume of coverage has multiplied fifty times.

The Public Demand

There are several good reasons for this amazing growth and expansion—all stemming from public interest and demand. The widespread distress of the depression years of the ‘thirties taught us many bitterly learned lessons. Uppermost was the lesson which led us to think very practically about the ways a man could best protect himself and his family against the devastating effects of another such period in the future. And a major part of personal and family security depends on protection against accident and sickness.

Employers, too, began to recognize health insurance as a necessary, in fact, a primary part of any program for developing sounder, more stable relationships with their employees. Organized labor, particularly during the wartime period of wage-freeze, turned to fringe benefits, especially health insurance, as desirable bargaining objectives.

Another contributing influence was the increasing complexity of health care, which by 1941 included oftentimes expensive professional specialization, employment of new and expensive drugs and equipment, and not only the greater use but the increasing cost of hospital facilities. All such factors had the effect of directing public attention to the high cost of ill health. Hospitals themselves have always been concerned with the payment of their charges—and doctors, zealous to preserve the private practice of medicine, encouraged their patients to be insured.

No one group or organization can claim credit for fulfilling—or approaching fulfillment—of all the public’s needs for protection against the cost of ill health. However, some indication of the part insurance companies of America played in serving the health insurance objectives of the public can be gained from the totals cited on health insurance coverage in 1956.

Of the 110 million who have hospital insurance, more than 60 million are insured by insurance companies. Included in the 94 million with surgical insurance protection are more than 57 million covered by insurance companies. In the area of general medical expense insurance where 58 million people are protected, insurance companies underwrite more than 25 million Americans. Insurance companies pioneered the major medical or catastrophic type of coverage which insured practically all of the seven million people who had this form of medical care protection by mid-1956. Of the nearly 40 million persons protected against loss of income, more than 30 million are covered through insurance company plans.

Flexible Planning

In providing for the public’s interest, the role played by insurance companies in 1941 and today does not of necessity follow a prepared script. This, in general, accounts for the reason public acceptance has grown so rapidly. The type of health protection desired and needed by a family in Delavan, Illinois, may be entirely different from the protection required by a department store clerk in Atlanta, Georgia.

Consequently, there must be a great deal of flexibility in insurance planning if health protection is to meet the requirements of individual interests, personal circumstances, and local conditions. It is this flexibility plus energetic reliance on the American tradition of free competition that has enabled the 800 insurance companies in this country to vie with each other in planning and providing the most acceptable insurance protections to fit the public demand. Some indication of the success with which these principles have been carried out might be gathered from the figures just quoted.

Basic Insurance Principles

While individuals differ in the types of health protection desired, and personal circumstances vary as well as local conditions, certain basic insurance principles are still applicable to all the millions of people who want personal and family health insurance protection. Though it performs a significant service for both the individual and the community, voluntary health insurance is simply a practical device for pooling or sharing a risk. Through it, a person substitutes a small certain loss—the premium paid-for a large uncertain loss—the wages forfeited and the expenses incurred because of disability. When a large number of people are about equally subject to the same risk of loss, and Lhe incidence of risk is fortuitous or beyond the control of the people to be insured, the insurance technique may be applied successfully.

Although much illness is subjective, and there are many problems of evaluating risk and substantiating loss by a person, family, or larger group, underwriters have pretty well perfected the process of insuring against most of the financial losses arising from disability. To the person insured, it means he can expect cash benefits in specified amounts for time lost from work because of illness or injury. Or his protection may take the form of cash benefits against expenses incurred because of necessary medical care during disability. In either or both events, the voluntary approach to health insurance gives the person the right to select what he desires. He can choose the amount and kind of benefits he wants to purchase within the broad limits of underwriting rules established to protect the whole body of people with whom he shares his risk.

To make this arrangement possible at a reasonable price for all within the group, another time-tested insurance principle is practiced. In health insurance a fundamental that is becomingmore apparent is that only the serious or financially crippling losses should be insured. Losses that are routine, recurrent, and trifling are financed much more economically as a part of the regular family budget like food, shelter, and clothing. Nearly everyone loses a day or two a year because of a scratch or sniffle and will spend a few dollars at the drug store for his favorite nostrums—or will have a physical checkup and visit his doctor. By eliminating these inconsequential and seemingly inevitable small losses through a deductible provision (similar to those found in automobile collision insurance), the buyer’s premium dollar is conserved to purchase more adequate coverage for the serious loss.

Another insurance principle of great importance to sound voluntary health insurance, and understandably acceptable to the vast majority of insured, is that the person holding health insurance protection for himself and/or his family should have a financial interest in the loss by bearing a part of it himself. This is called “co-insurance.”

The purpose of this principle is to discourage the possibility of utilizing unnecessary and extravagant services and care in gaining recovery, for, as a logical result of the risk-sharing principle, if no consideration were given to the extent and costs of unnecessary service and care, widespread adoption of a “shoot-the-works” attitude would mean increased premiums for the entire group sharing in the protection.

Broader Coverage for More People

These, then, are the basic principles used by insuring organizations to meet the public demand for such health insurance as it wants to select. As has been mentioned above, the broad fields of coverage designed to meet the demand include protection for hospitalization, general medical expense, surgical expense, and loss of income due to disability. And while great progress has been made in voluntary health insurance to serve the public interest, it has not yet reached every segment of the population. Those who cannot pay the relatively modest cost of insurance are beyond its reach. Happily, they are a sharply declining percentage of our growing population. Their care is now, as it always has been, a proper charge against the entire body politic and is best and most economically provided by direct assistance, locally administered through the established agencies of government.

Millions of Americans, many of them in the lower income brackets, are assisted in seeming voluntary health insurance on a group basis through the contribution of their employers. Splendid advances are being made in the provision of insurance for the aged. Most insurance companies have raised the age limits for continuing the coverage of their policyholders and for the issuance of policies to new applicants at older ages. Increasingly, group contracts permit a continuation of coverage to retired employees and their families while some policies provide “paid-up” benefits at retirement.

Many physically impaired persons can now buy health insurance with premiums adjusted according to the severity of the impairment. Substantial numbers of people in sub-standard health are insured at regular rates under group policies which do not require individual evidence of insurability. People living in rural areas are being reached much more effectively than ever before.

There is still a great deal to be clone to fulfill the health insurance requirements of our population. Perhaps the most significant stride that has been made in recent years has been the allencompassing health protection offered by major medical insurance. It, too, has been subject to many changes, additions, revisions, to fit public interests. In its present stage, it provides the major share of payment for substantially all the costs resulting from medical, surgical, hospital, drugs, appliances, and the “incidental” charges brought on by a big medical bill running into the hundreds or thousands of dollars. This is the plan which has the seal of approval of seven million people who have subscribed to it after its introduction six years ago.

Guides for the Future

Voluntary health insurance of the future will unquestionably be based on principles which have accounted for its spectacular growth in the past sixteen years. There will be public demands and increased interest—it will He up to the insuring organizations to continue answering and serving the public needs.

One thing is certain, the public’s demands and the response made by insuring organizations dearly indicate voluntary health insurance is America s answer to the problem of financing health care costs on a “pick and choose” basis without regimentation of the individual, the subordination of the medical profession to the state, or the standardization of a health insurance panacea handed to the public in a “take-ithecause-it’s-good-for-you” package.

[Additional copies of “Health Insurance and the American Public” are available from the Health Insurance Institute, 488 Madison Avenue, New York 22, New York.]